Navigation

Navigation

What is an Initial Exchange Offering: Must Read Guide

|

|

Initial Exchange Offerings, or “IEOs,” have been called everything from the second coming of the initial coin offering, a.k.a. “ICO 2.0,” to the next “killer app.” In the first half of 2019, they have already caused quite a stir among those active in the cryptocurrency community. So, what exactly are IEOs and do they live up to the hype?

Introduction

Before answering the question—”What is an IEO?”—it will be useful to provide historical context, especially for anyone who is not familiar with the cryptocurrency industry. This history lesson will include a quick review of initial coin offerings, or “ICOs.”

The ICO

The Beginning

There is some disagreement as to which was the “first” ICO, but J.R. Willett, founder of Mastercoin (which utilized the ICO fundraising method), is most often credited as being the inventor of the ICO, which he described in “The Second Bitcoin Whitepaper,” published on January 6, 2012. The basic format for the ICO has not changed very much since then:

- The founder or team set up a “trusted entity” (e.g., a corporation) to manage the ICO;

- The trusted entity publishes a Bitcoin, Ethereum or another cryptocurrency address where anyone who wants to participate in the ICO can send cryptocurrency;

- The trusted entity publishes the exchange rate for the new tokens or coins that it will be issuing for the ICO;

- The trusted entity publishes the closing date for the ICO;

- Anyone sending cryptocurrency to the addresses published in #2 before the deadline in #4 will receive the number of new coins or tokens as calculated per #3.

The above-referenced method worked well for many subsequent ICOs, including the ICO for Ethereum, which occurred on July 22, 2014. However, it was not until Ethereum’s ERC-20 token standard was published on November 22, 2015, that ICOs really began to take off.

That is because, thanks to ERC-20, it was now possible for projects to not only issue tokens easily, but they could be automated with smart contracts and, perhaps most important of all, the tokens could be stored in any ERC-20-compatible wallet. Together, this allowed projects launching ICOs to automate nearly all of the steps appearing above as well as include a much larger audience—basically anyone who had a single wallet that was compatible with the ERC-20 token standard could participate in any ICO. If you’d like to learn more about the ERC-20 token standard, you can also check out this Video Guide: What is an ERC 20 Token?

The Boom

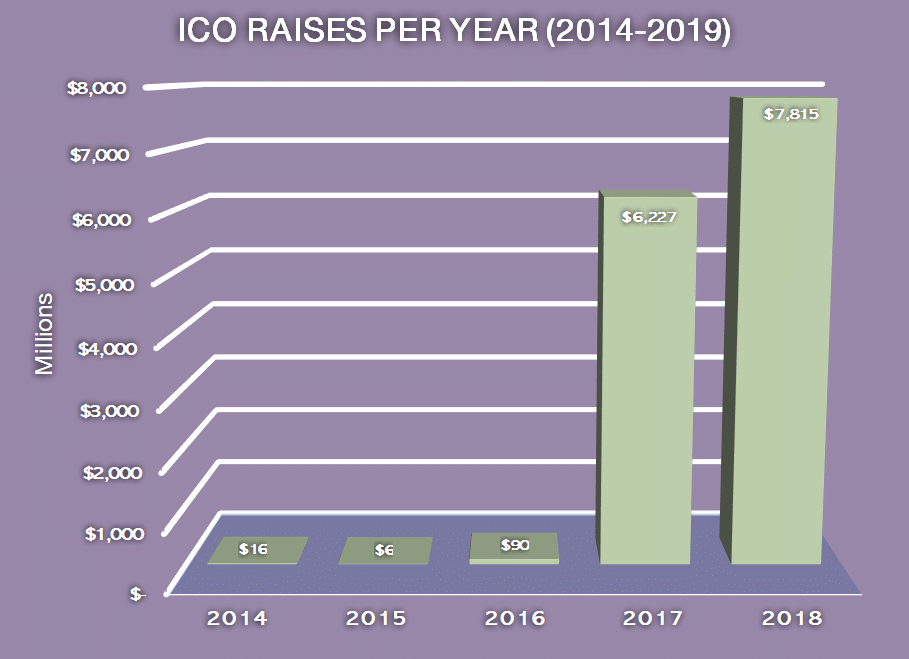

Prior to the release of ERC-20, the total amount raised via ICOs between 2014 and 2015 was approximately US$22 million. In 2016, it climbed to US$90 million. But as the chart below clearly demonstrates, 2017 was the year when ICOs really caught fire, raising US$6.2 billion. 2018, the final year of the ICO boom, saw a total raised of US$7.8 billion. So much money was being brought in via ICOs that an entire support industry grew up around them. But as anyone familiar with the laws of physics (and economics) knows, what goes up always ends up coming down.

The Bust

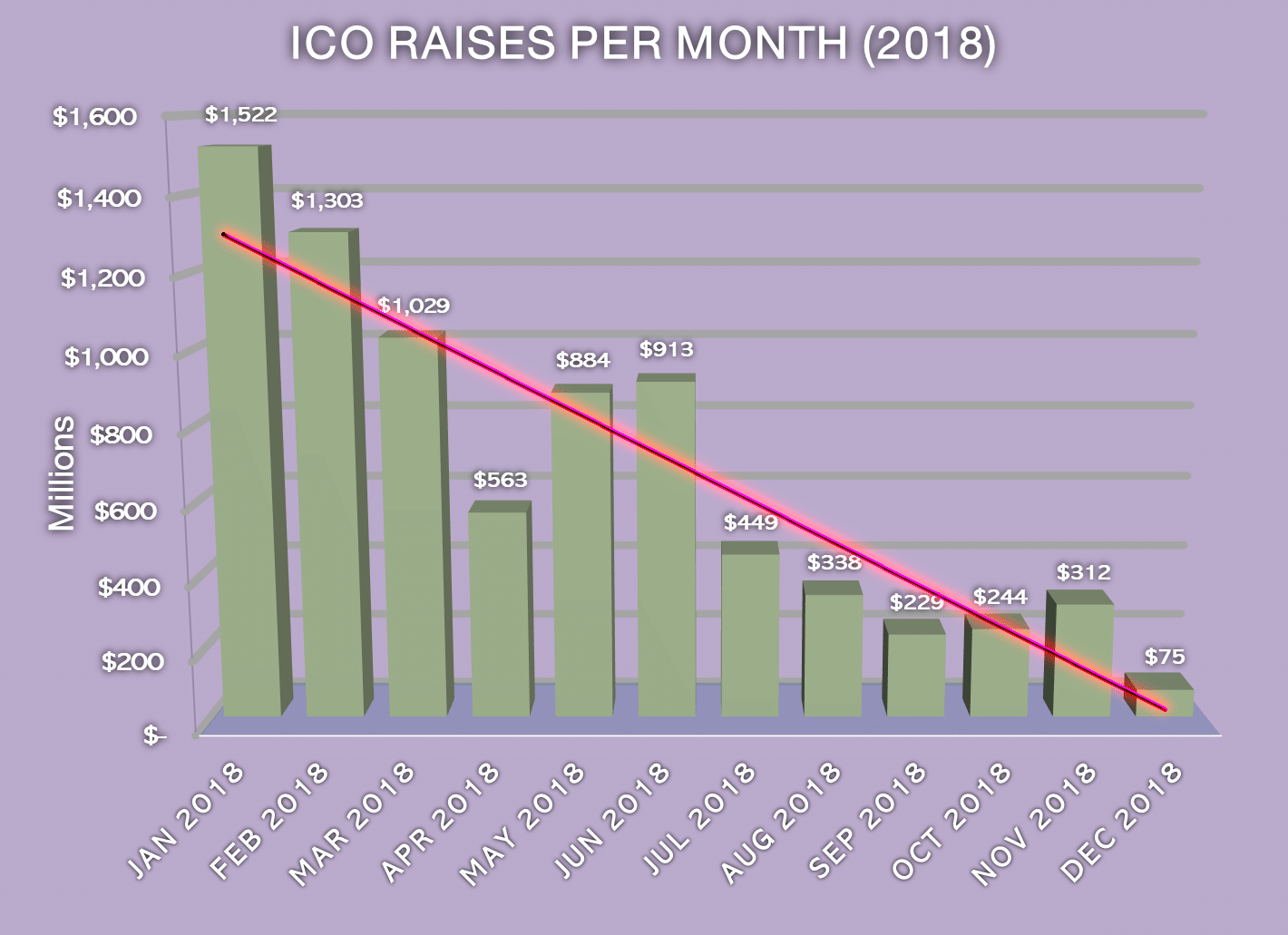

Although when looked at year-to-year, 2018 was a banner year for ICOs (raising an incredible US$7.8 billion according to ICOdata.io), when looked at month-to-month, 2018 was a miserable year. From a high of US$1.5 billion in January, the chart below shows a trendline predicting a collapse in December, which is exactly what happened. To add insult to injury, information came to light that many projects had engaged in “interproject token swaps,” where one startup raising funds swapped its tokens with another project and both claimed the value of the tokens based on the closing price of each other’s ICO. In short, the ICO boom had completely busted by the end of 2018.

What Happened?

There are different theories as to exactly why the ICO market imploded as quickly as it began. It is safe to say, however, that at least two factors were involved: (1) many (if not most) of the projects raising funds were simply not very good; and (2) the theory behind the ICO as a sound investment was flawed, meaning that the incentives of startups and investors were completely misaligned and the only real winners were investors who could manipulate the markets to their advantage. In retrospect, the collapse should not have been much of a surprise, as the multitude of problems with the system were all well-documented by independent bloggers and journalists within the industry:

- The American ICO is Dead by Preston Byrne (March 7, 2018).

- ICObench Warmer by Tokenicide! (April 24, 2018).

- This Is How Easy It Is to Buy ICO Ratings — An Investigation by Markus Hartmann (Jun 14, 2018)

- We Asked Crypto News Outlets If They’d Take Money to Cover a Project. More Than Half Said Yes by Corin Faife (October 25, 2018).

And of course, the mainstream media contributed its fair share of warnings as well:

- Buyer Beware: Hundreds of Bitcoin Wannabes Show Hallmarks of Fraud by Shane Shifflett (May 17, 2018).

Impact on Exchanges

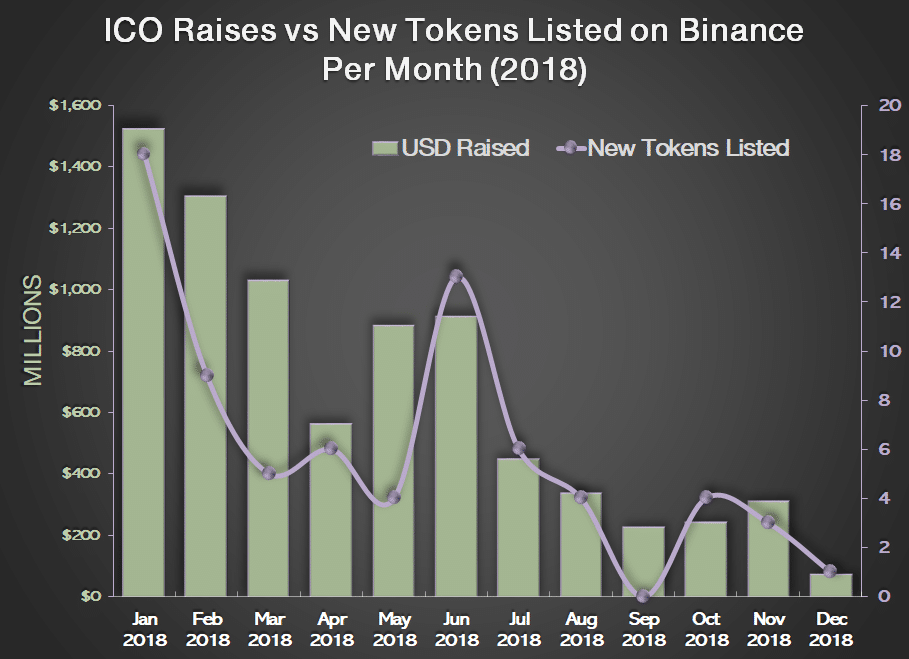

At the height of the ICO boom, rumors started circulating that some major exchanges were demanding up to US$1,000,000 or more to list a token that had been sold via an ICO. As the number of ICOs reaching their targets and the amount each was raising began to take a nosedive, so too did the funds available to list tokens, meaning that fewer and fewer tokens were bothering to get listed. As an example, the chart below shows how the amounts raised by ICOs (the green bars) impacted the number of new tokens being listed on one of the most popular cryptocurrency exchanges in 2018. Although it is not a perfect correlation, the general trend is the same. In September of 2018, the exchange in question did not list ANY new tokens. To suddenly go from several million dollars per month to zero must have been a serious wakeup call and would incentivize exchanges to find “the next big thing.”

The IEO

Given the lack of listing fees coming into the exchanges, it only made sense that they would produce another way to increase their revenue. The IEO fit the bill perfectly.

History of IEOs

Although IEOs have only recently landed in the spotlight, the first two IEOs are typically considered to be GIFTO and Bread, both of which were launched in November of 2018 on the Binance Launchpad. It is therefore no surprise that Binance has been the primary force behind its resurgence. So, what exactly makes an IEO an “IEO?”

What is an IEO?

If you recall the previous description of ICOs, the first step in setting one up is to establish a “trusted entity.” In the case of ICOs, the trusted entity would be the corporation or other legal entity (i.e., the startup) that the founding team established to run the ICO. In the case of IEOs, the trusted entity is a cryptocurrency exchange. That is the only substantive difference. One may therefore wonder what is the big deal and why are they so popular? The answer is that by hosting on an exchange, IEOs offer benefits that ICOs lacked:

IEO Benefits

Here are the most often cited benefits to IEOs:

Tokens are Immediately Tradable

A recent study showed that less than 10% of ICOs went on to list their tokens on an exchange. Since this was the primary motivation for most investors to participate in ICOs, it is understandable that this would be a very frustrating result for them. IEOs correct this problem by baking in the fact that immediately upon the close of the token sale, the tokens will be available to trade on the cryptocurrency exchange that is hosting it. This provides the much needed or hoped for liquidity that so many ICOs failed to deliver to their investors on.

Projects Hosted by Exchanges Are More Legitimate

Even setting aside for a moment the outright scams that were prevalent during the boom and bust of ICOs, one of the biggest complaints about ICOs (as cited above) was the fact that very few of them were viable as a business. The argument goes that exchanges have an incentive to not list projects that are low quality because they have a brand name which needs to be maintained.

Less Noise

The third and final benefit to IEOs compared to ICOs is the fact that unlike the height of the ICO boom, when it seemed that everybody and their cousin was trying to launch an ICO, at the present time IEOs are still relatively rare by comparison. So, if a project has the good fortune of being listed on one of the major exchanges, that by itself will put it head and shoulders above all others and guarantee traction that would be very expensive to get otherwise.

Criticisms of IEOs

As mentioned above, the fact that the trusted party for an IEO is an exchange as opposed to a fly-by-night company that may have not even existed a week prior to the token sale (as happened periodically in the case of ICOs), is a very important distinction in IEOs’ favor. However, despite their recent popularity, there have been many criticisms of IEOs, including the following:

IEOs Benefit Exchanges

There is no serious debate about the fact that IEOs were created by exchanges, for exchanges, as a response to the ICO crash, as discussed above. As a result, it should come as no surprise that IEOs benefit exchanges. In addition to requiring substantial listing fees in some cases. The author has already seen listing agreements with the following requirements:

- Fees in excess of US$200,000;

- A substantial % of the funds raised during the IEO will be locked by the exchange;

- A requirement that the token price must stay above the launch price for at least a month; and

- A requirement that the token maintain over US$1 million in daily volume on the exchange otherwise the exchange could delist the token and take all of the aforementioned amounts as a security payment.

IEOs Are More Likely to Violate US Securities Laws Than ICOs

On May 13, 2019, the U.S. Securities and Exchange Commission’s Advisor for Digital Assets and Innovation, Valerie Szczepanik, warned exchanges that requiring a fee to launch and list IEO tokens might subject them to broker-dealer regulations in the U.S. As a result, if the IEO involves the sale of a security (as defined under U.S. law) and either the token issuers or any of the buyers are from the U.S., the exchange would be in violation of the law if they were not properly registered in the U.S.

At first glance, this is no different than the problems exchanges and token issuers had to face with ICOs, because the ultimate question is whether the IEO involves the purchase or sale of a security. However, one of the factors considered by the SEC in determining whether something is a security is whether a “purchaser may expect to realize a return through participating in distributions or through other methods of realizing appreciation on the asset, such as selling at a gain in a secondary market.” If you recall the primary benefit of IEOs is the fact that immediately upon the close of the token sale, the tokens will be available to trade on a secondary market, which is exactly what investors expect. As a result, in this author’s opinion, IEOs by their very nature are more likely to involve the sale of securities than ICOs.

IEOs Do Not Fix Misaligned Incentives

In this author’s opinion, IEOs make the most fundamental flaw in ICOs even more pronounced, namely, something called “misaligned incentives.”

One of the things that made ICOs so attractive to founders was the fact that founders did not have to give up any equity in the underlying business. The same is true of IEOs (at least all of the ones the author has reviewed). The reason this is a problem is because without equity in the underlying business, investors don’t actually care about the business. All they care about is the token. And there is no incentive to prevent them from dumping the token to make a quick profit, even if it kills the business, because they have no equity in it. These are the “misaligned incentives” mentioned above.

IEOs not only fail to fix this, but they make it even more pronounced by acknowledging that the token (by being listed on the exchange) is the only thing that matters.

Are IEOs Worth Investing In?

Not being a financial advisor, I cannot comment on whether someone should invest in IEOs. But what I can say is that because an IEO is merely a fundraising method, deciding whether IEOs are sound investments is kind of like deciding whether “stock” is a sound investment. It can be, but it ultimately depends on the company issuing the stock. The point being that if you are seriously considering investing in an initial exchange offering make sure you know exactly what it is you’re investing in. At the end of the day, you must do your own independent research and conduct due diligence. And no matter what, never invest more than you can afford to lose.

If you’d like to get in touch with the author, Grant Gulovsen:

• Email: mailto:grant@gulovsen.io

• Facebook: http://facebook.com/gulovsenla

• Instagram: https://instagram.com/gulovsen

• LinkedIn: http://linkedin.com/in/gulovse

• Medium: https://medium.com/@gulovsen

• Twitter: http://twitter.com/gulovsen

• Website: https://gulovsen.io

• YouTube: https://www.youtube.com/channe

The audio is not working.

The audio is not working.

The audio is not working.

Glad you liked it.

Glad you liked it.

Glad you liked it.

Very informative appreciate the information,

Thanks. Glad you liked it.

Very informative appreciate the information,

Thanks. Glad you liked it.

Very informative appreciate the information,

Thanks. Glad you liked it.