Contents

|

|

Ranging from investment within the capital markets to the provision of credit by institutions, the concept of financing, at its core, aims to provide the finances with what he doesn’t have in general or temporal terms. It is a concept which is a long-standing technique availed of by the masses for reasons which are personal and customized to one’s profession, interests and social standing.

If one had to look at different sources of financing, whether such sources are against the backdrop of a filial relationship or whether such financing is against the backdrop of a contractual relationship with a financial institution, it immediately becomes evident that the concept of ‘trust’ dominates any financing arrangement which any person would enter into. By way of example, if a teenager was to borrow money from his brother, the brother lending the money does so on the basis of the fact that he knows his brother and trusts that he will be repaid in the future. Similarly, and perhaps more surgically, a financial institution will only approve a mortgage on the basis of it having the knowledge that the borrower has proved that he has the financial capacity and capacity to repay the financial institution in the future. The financial institution, on the basis of its own examination process, is led to a point where it ‘trusts’ that the borrower will not fall short in the performance of his obligations.

It is, therefore, no surprise that the concept of financing has evolved with the emergence of technologies that have proved to provide comfort, from a trust point of view to all parties involved in a financing transaction. Blockchain technology is an example of one such technology. It is also perhaps safe to say that bureaucratic legal practices that are part of the ‘baggage’ of seeking or granting financing have elevated.

The purpose of this piece is to provide the reader with a brief flavour as to the advantages and challenges which microfinance, particularly the provision and acceptance of micro-loans, pose to all parties involved.

Contents

Virtual Financial Assets And The Regulation of Blockchain Micro-Loans

Access to the financial system goes a long way when determining one’s social standing. It is indeed such social standing which, for better or for worse, determines the way an individual lives his life. At its core, the concept of financial inclusion strives to ensure that the main routes of exclusion to the financial system are eliminated through the implementation of infrastructure, law and policy. Exclusion may come in various forms such as price exclusion, whereby the price one has to pay for access to the financial system is not affordable and access exclusion, whereby the location or infrastructure where one is based does not permit access to the financial system.

The concept of financial inclusion is, therefore, one which may be viewed and interpreted from different lenses and in its definition, is embedded with a sense of elasticity that adapts to the mentality and self-set standards of any person pronouncing himself on the matter. What is certain is that at the very heart of every opinion as to what financial inclusion is (or is not), the elements of the need for a minimum standard of education, affordability and state-development/encouragement to avail of socio-friendly financial systems reverberate and rebound against the walls which encapsulate any and all attempts to define the matter.

Undoubtedly, law plays a huge role in ensuring that the financial system is not only delivered to the end customer at the highest possible standard and with the most robust of safeguards, but it also plays a critical role in ensuring that the financial system is accessible to the public at large.

The ‘microloans/credit’ concept

As the name implies, when we speak of ‘micro’ we speak of small and limited capacity. Indeed, the ‘limited’ nature of the concept alludes to the lower end of the pyramid and financing too and amongst persons who fall within that spectrum. Inevitably, therefore, the figures in micro-finance are, when compared to the concept of ‘finance’ in general and more wide-ranging terms, low.

The roots of the concept date back centuries, however, one notable mark in modern microfinance was when Muhammad Yunus, in a time when famine swept Bangladesh, loaned minimal amounts of money to women in Bangladesh for the latter to be able to develop their own produce. The loans were not collateralized, and this meant that the lower earners within the Bangladesh society had access to a financing facility in pursuance of growing their own business, as small as the latter may have been. This model hence combatted the exclusions to financial exclusion as denoted above.

The novelty of the concept invariably attracted the attention of entrepreneurs and established financial institutions which saw business opportunity in the concept, that is to say, the concept of micro-finance, particularly micro-credit, proved to be an additional tool which may be added to an up and coming or already established financial institution’s business model, generating a revenue stream.

The legal position: Focus on Malta

From a reading of Article 3 of the Financial Institutions Act (Chapter 376 of the laws of Malta), it can be deduced that no person may regularly or habitually, in or from Malta, provide services tantamount to “lending (including personal credits, mortgage credits, factoring with or without recourse, financing of commercial transactions including forfaiting)” unless such activity is channelled through a corporate vehicle and unless such company holds a licence duly issued by the Malta Financial Services Authority (the “MFSA”) which allows it to perform such activity and hence, provide such services. In this respect, the same Act defines a “credit facility” as “the lending of a sum of money by way of an advance, overdraft or loan, or any other line of credit, including discounting of bills of exchange and promissory notes, guarantees, indemnities, acceptances, bills of exchange endorsed pour aval and financial leasing”. It is evident, therefore, that the provision of a micro-loan in fiat is considered to be a regulated activity that requires the service provider to be in possession of a valid licence issued by the MFSA (or equivalent authority in terms of European Union law).

It is also to be noted that when a person conducts the “business of banking” in terms of the Banking Act (Chapter 371 of the Laws of Malta), which in a nutshell, is inclusive of accepting deposits of money from the public and lending out, in whole or in part, such deposits to other clients of the business, needs to duly be in possession of a valid licenced issued by the MFSA.

Therefore, whether a person is lending money from its own reserves or from pools of deposits accepted from the public, law mandates that such entities must seek authorization and must hence submit themselves to supervision.

Restrictions and exclusions

Firstly, one must not forget that the regulation quoted above is limited in application to the lending of money, the latter of which is best embodied in what we know as ‘fiat currency’. Interestingly, and very intelligently, the law does not specifically define what ‘money’ is, keeping the concept as open-ended which needs to be interpreted in terms of the socio-economic present in and any legal conditions which are in force at a specific moment in time. By deduction, we can safely say that irrespective of whether money is physical, digital or electronic, insofar that it satisfies what is economically and legally acceptable as money, it will be deemed to be subject to the abovementioned restrictions when availed of in a lending transaction.

From a pure fiat currency perspective, the Financial Institutions Act as above referenced also includes numerous exemptions as to when a licence is not required. For example, in terms of the Financial Institutions Act, an entity is not deemed to be conducting the business of a financial institution, and hence, a licence is not required, if lending occurs between entities which form part of a group of companies or if such companies are all controlled, directly or indirectly by the same person.

Virtual Financial Assets: an opportunity?

Following the aforementioned determinations, it only seems natural that a question which any inquisitive person would ask is “What if you lend cryptocurrency?”. An answer to such a question needs to set off, in terms of local Maltese law, as to what a ‘cryptocurrency’ or, as coined in Malta, a “Virtual Financial Asset” (VFA), really is. The answer to such lies in the Virtual Financial Assets Act (Chapter 590 of the Laws of Malta), wherein a VFA is defined as “Any form of digital medium recordation that is used as a digital medium of exchange, unit of account, or store of value and that is not (a) electronic money (b) a financial instrument; or (c) a virtual token”. Insofar, therefore, that an asset is not considered to be electronic money in terms of the Financial Institutions Act, a financial instrument in terms of the Investment Services Act (Chapter 370 of the Laws of Malta) and a virtual token in terms of the Virtual Financial Assets Act, then such an asset, provided that it is a form of digital medium recordation which is capable of being deployed as a medium of exchange, unit of account or store of value, such an asset is deemed to be a VFA. The lending of an asset classified as electronic money will be subject to the abovementioned treatment in terms of the Financial Institutions Act or the Banking Act (depending on the specific intricacies of the business model in question).

Opportunity knocks, however, for a more flexible lending arrangement when the asset being lent out to a borrower is one which is classified as a VFA, simply because the VFA Act in itself does not regulate the activity of “lending” such virtual tokens or VFAs, and VFAs are capable of being traded for other VFAs or exchanged for fiat money. Within the context of the real world, conversion by the borrower of a VFA of that VFA into fiat money, provides such a borrower with an opportunity to avail of such money for his or her personal development. Therefore, indirectly, the micro-credit arrangement expounded by Muhammad Yunus as noted above, which, in its purest form, is subject to regulatory approval, may still be achieved without the need to subject the lender to the bureaucratic regulatory processes associated with Financial Institutions and Banks. Of course, lack of exposure to such processes depends on the intricacies of the ‘loan arrangement’ in question, which shall be discussed in the subsequent section of this piece.

Of course, some may say that the above is not a novel concept and maybe effectively implemented using any form of asset (for example: borrowing four apples, selling them for a value in fiat and using that fiat).

Loans of VFAs

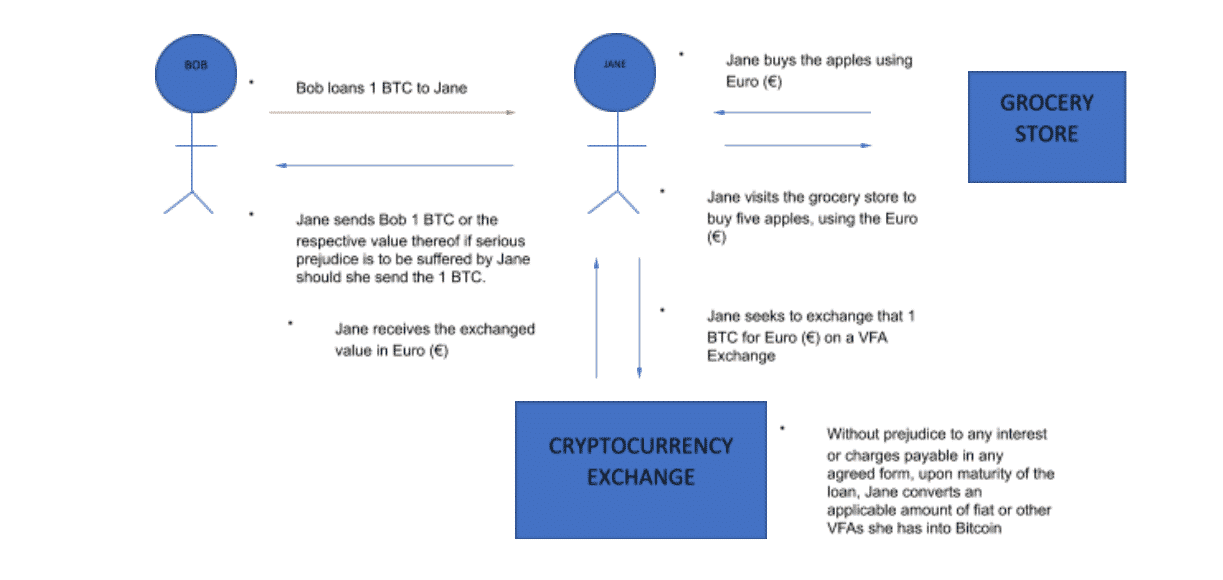

As denoted above The Virtual Financial Assets Act does not regulate the lending activity, in whatever form, of VFAs i.e. the Act does not regulate the activity of when a person lends out his or her VFAs to another person, but limits itself in application to the intermediaries involved (i.e. VFA exchanges, brokers, custodians, etc) and issuers of such VFAs. The act of loaning a VFA from one person to another, for the other to be able to use such a VFA as agreed between the parties would classify as a loan for consumption in terms of Maltese law, provided that the initial VFA loaned out is returned to the lender. Law makes provision for the possibility of the loan to be repaid in terms of the value of the VFA loaned out at the time and place the loan was made (unless agreed otherwise) if serious prejudice is to be suffered by the borrower should he seek to return the VFA in the same kind and quality it was loaned out. The charging of interest on the loan is not automatically allowed and must be specifically catered for in the loan agreement in question. Should interest be charged, the rate of interest cannot exceed that of 8% per annum. If a rate of interest is not agreed upon but it has been agreed that interest is to be charged, the law specifies that a 5% rate shall apply. Figure 1 below provides a graphic overview as to how such an arrangement may be achieved through a borrower’s independent use of a third-party cryptocurrency exchange.

Figure 1: An example of a VFA loan within the context of a loan for consumption:

The future of blockchain in micro-credit

On a critical note, it should be expounded that availing of VFAs for the purpose of micro-credit may not necessary be the wide-ranging solution, simply because, as of today, access to virtual financial assets exchanges, brokers and intermediaries as well as knowledge and trust in virtual financial assets is a long way from mass adoption and acceptance.

The power of blockchain technology may, therefore, be better utilized through implementation for the fiat model. Nonetheless, lending of VFAs to persons which are (a) able to access the VFA ecosystem and (b) willing to borrow such VFAs from willing lenders remains an option.

Blockchain is borderless and at its peak, may also connect borrowers with lenders without the requirement of financial institutions. Of course, the law would need to allow for the discard of such intermediaries. Through immutability and openness, it is clear that blockchain and blockchain-based assets have the potential to trigger a micro-finance revolution, however, such optimism needs to be neutralized by proper and ethical development of the technology through education and development which on the one hand challenges the applicability of currently enforced laws whilst on the other hand, ensures that law and the spirit of the law is not breached or disregarded.

Thank you for the report!